Category: News

-

Suretyship under the new Book 9 of the Belgian Civil Code: a familiar “nest egg”, clearly and modernly redefined as of 1 January 2026

In this newsletter, we highlight the main features and changes relating to this security technique. The rules have not fundamentally changed; they have primarily been modernised and clarified. It is essential to understand these rules properly: anyone who enters into a suretyship may face significant consequences for their personal assets. Knowledge of the new legislation…

-

PEPPOL COUNTDOWN: Are you ready for e-invoicing in 2026?

Despite extensive information campaigns, it appears that less than half of Belgian businesses are currently compliant with the new statutory obligation. Failure to switch in time, may, as from 1 January 2026, result inter alia in: The Federal Public Service Finance (FPS Finance) has, however, recently announced the introduction of a tolerance period of three…

-

Late-filed documents may alter the outcome of the permitting process

CPD 23 October 2025 (RvVb-A-2526-0131) 1. Which situation prompted the decision? A project for the construction of nine single-family homes in an inner area, had previously led to three annulments by the Council for Permit Disputes. In the fourth round, just before the hearing at the Provincial Authority, the applicant submitted an additional noise study…

-

Personal securities that may affect the deal

The reform of Book 9, Title 1 of the Civil Code modernizes the previously fragmented framework governing personal securities and introduces greater structure. For M&A-transactions, this results in increased legal certainty during due diligence and in the drafting of transaction documents: the validity, duration and scope of such securities may now be assessed differently, which…

-

The introduction of Title 1 of Book 9 of the Civil Code provides an important facelift to the law on personal securities.

With the introduction of this new Code, the legislator takes a major step toward modernizing property law. Although the remaining titles – including those on pledge, mortgage, retention of title, right of retention, and privileges – will follow later, this first title already forms the core of a more coherent regulatory framework. Personal securities, in…

-

Permanent residence not a condition for inclusion of a dwelling in the permit register

Judgment of the Council for Permit Disputes (RvVb) of October 2, 2025, no. RvVb-A-2526-0072 What is the permit register? Every Flemish municipality is required to maintain a permit register. This is a digital database in which information about spatial planning is collected for each plot of land. For example, you can find out which permits…

-

No financial charges may be imposed in an environmental permit without an urban planning regulation.

Decision RvVb 9 October 2025, No. RvVb-A-2526-0090 What is a financial charge imposed in connection with an environmental permit decision? A financial charge is an additional obligation imposed in the context of an environmental permit, under which the applicant pays an amount to compensate for the impact of the permitted project. This amount may then…

-

Proposed decree: EIA screening transferred to higher government

From ‘judge and jury’ to a more independent assessment In our previous contribution, we pointed out the fundamental tension that arose when local authorities had to assess their own projects entirely on their own. The Court of Justice (May 8, 2025) and the Constitutional Court (September 18, 2025) have since confirmed that this is contrary…

-

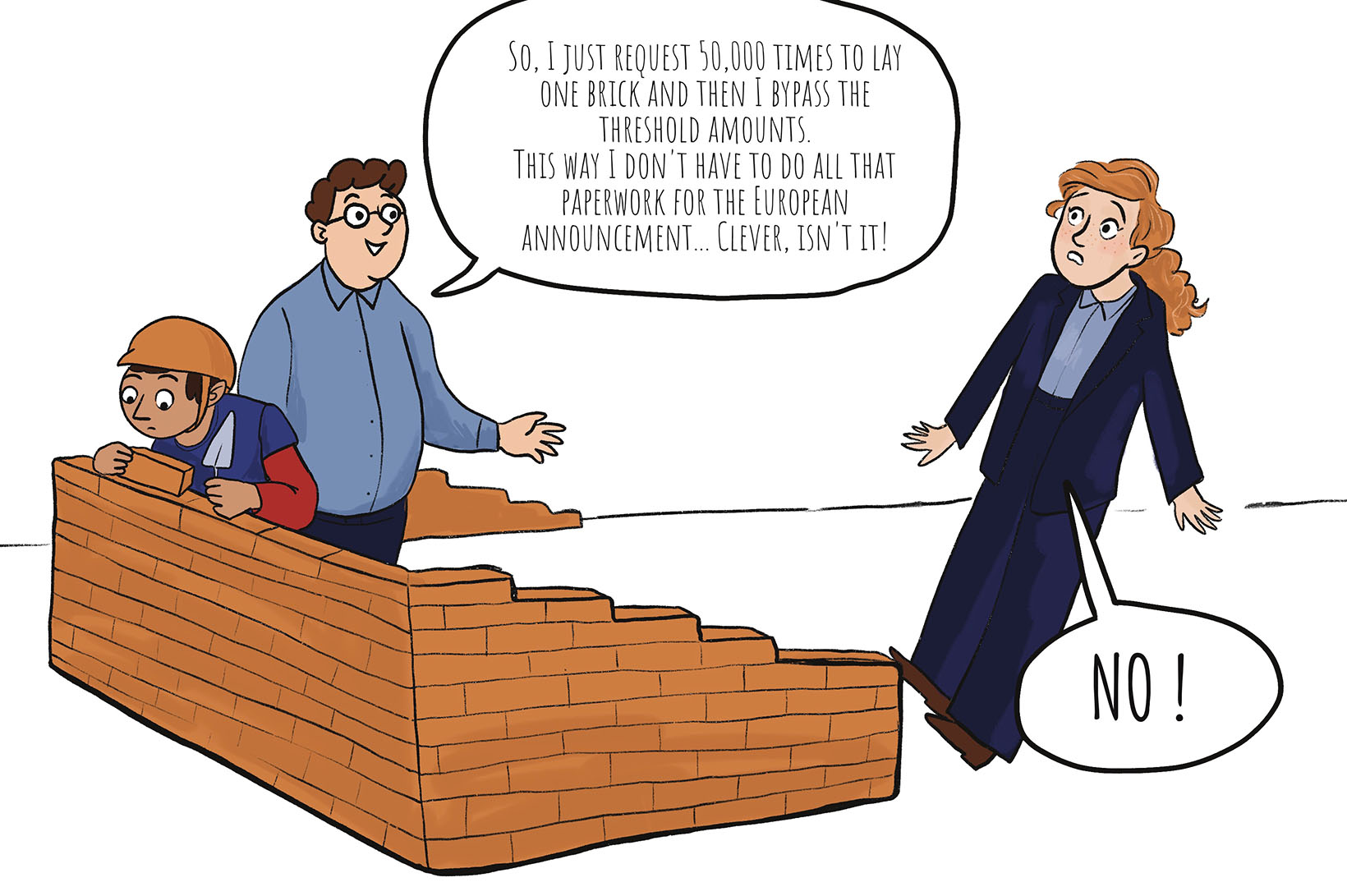

Tightening of public procurement regulations following new European threshold amounts from January 1, 2026

The European threshold amounts indicate whether or not a public procurement is subject to the European regime, and in particular to the European rules on publication, references in the tender documents, remedies, etc. Public procurements with an estimated value equal to or higher than the European thresholds will be subject to European publication. This means…

-

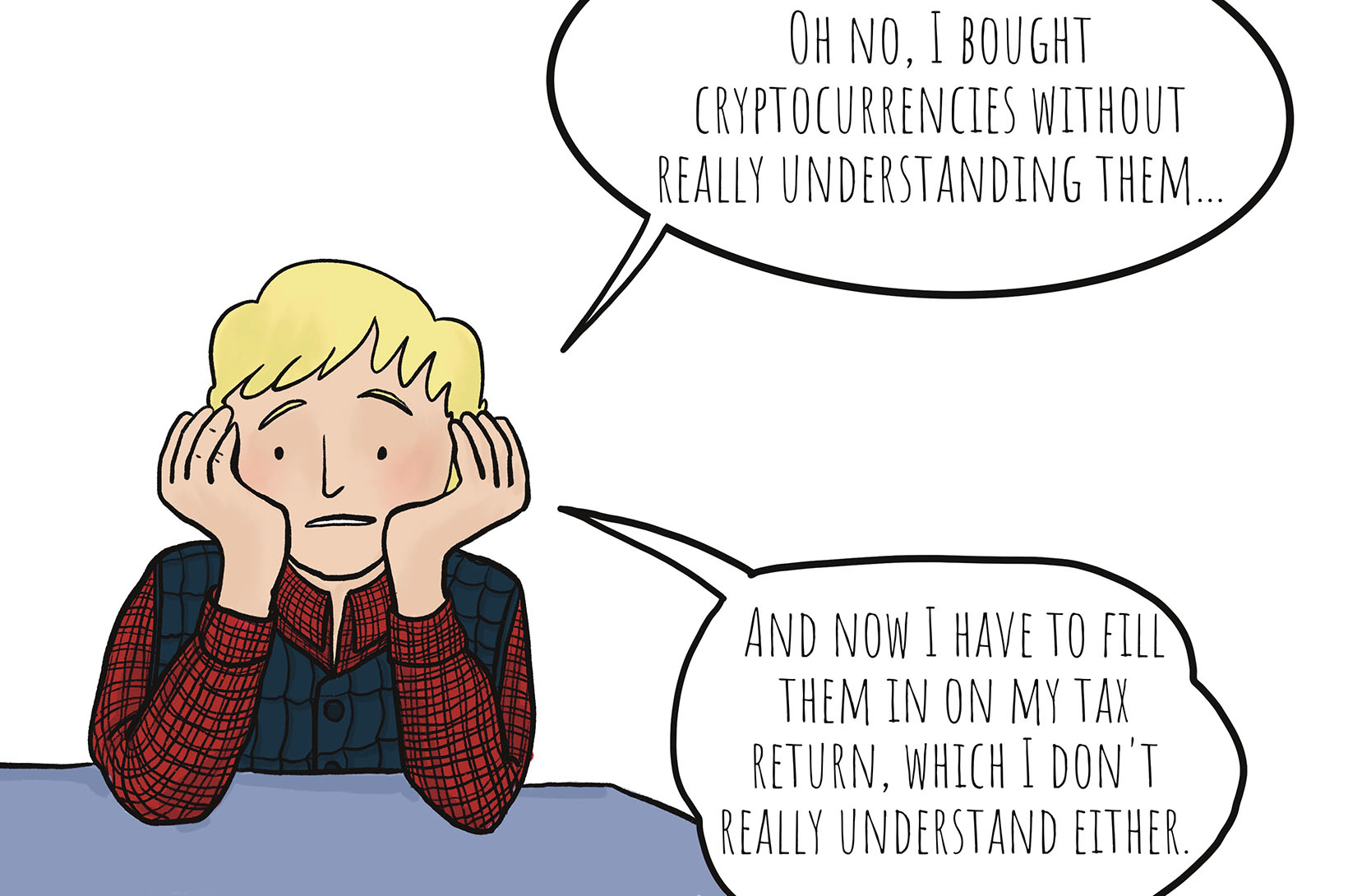

Tax challenges for cryptocurrency investors

Under current Belgian tax legislation, capital gains realised by individuals on cryptocurrencies may either be exempt as part of the normal management of private wealth, taxed as miscellaneous income at a separate rate of 33%, or – in cases of a regular and organised activity – taxed as professional income at progressive rates. Recent practice…